.svg)

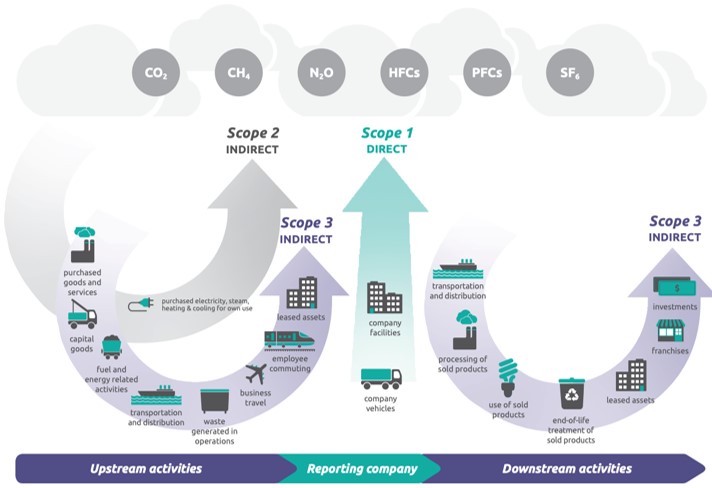

Scopes and emissions, according to the Greenhouse Gas Protocol

The GHG-P classifies corporate emissions according to different business processes called Scopes.

- Scope 1 includes the direct emissions from sources owned or controlled by the company, such as transport and premises.

- Scope 2 covers indirect emissions from purchased electricity, heating and cooling.

- Scope 3 considers indirect upstream and downstream GHG sources in a company’s value chain that are not owned or controlled by the company.

Source: Greenhouse Gas Protocol

Do you want to know more about our solutions to reduce emissions? Let's have a chat.

Get in touch

Peter Bloor

Director of Corporate Sales